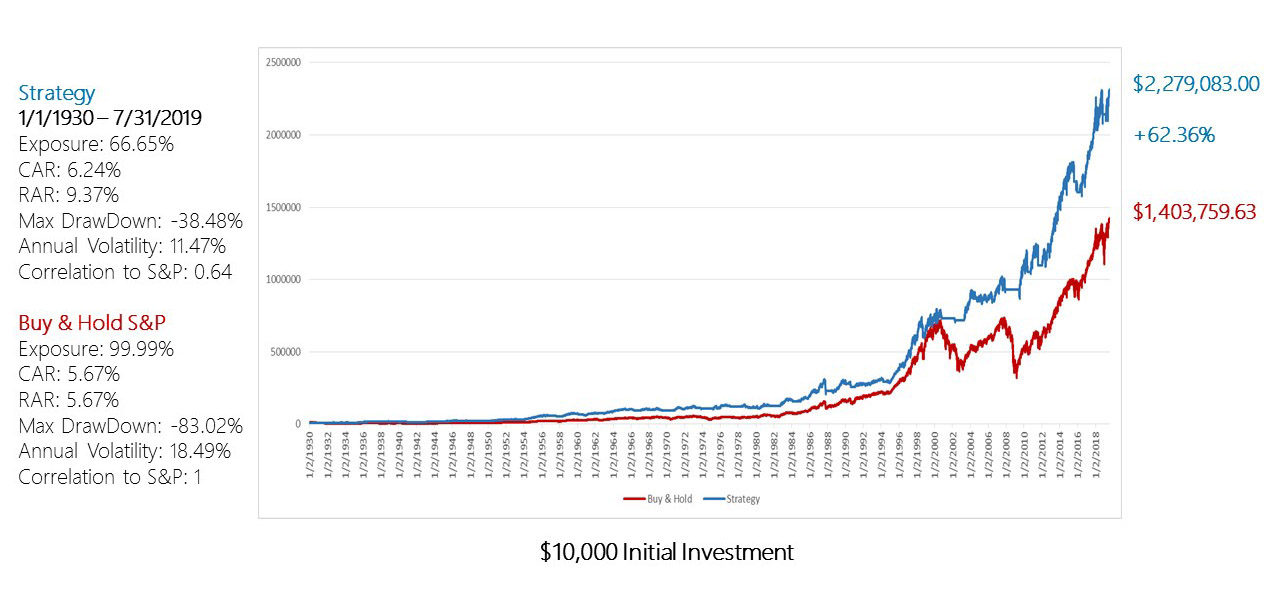

Our goal was to test our quantitative strategy both historically and more recently. In order to do this, we decided to backtest the strategy by applying it to the S&P500 versus the S&P500 invested 100% of the time (Buy-and-Hold). The charts below show the backtested results of our proprietary portfolio management strategy and investment process from the 1930s to 2019 and 1991 to 2019. The results demonstrate the effectiveness of our process in both making money in bull markets and protecting capital in bear markets. Portfolio managers bring value-added when they can successfully do both for their clients. With our strategy, our clients are able to outperform with less risk and market exposure (risk-adjusted return, RAR).

Making Profits & Protecting Capital Can Be Done

1/1/1930 – 7/31/2019

If an investor would have invested $10k in January 1930 through July 31, 2019, he or she would have outperformed the benchmark S&P500 Index by 62.36% with substantially less risk and market exposure (annual volatility, max drawdown, RAR). So, protecting capital and making profits can and should be done. There is no need to be invested 100% of the time through a Buy&Hold strategy that adds no value to investors.

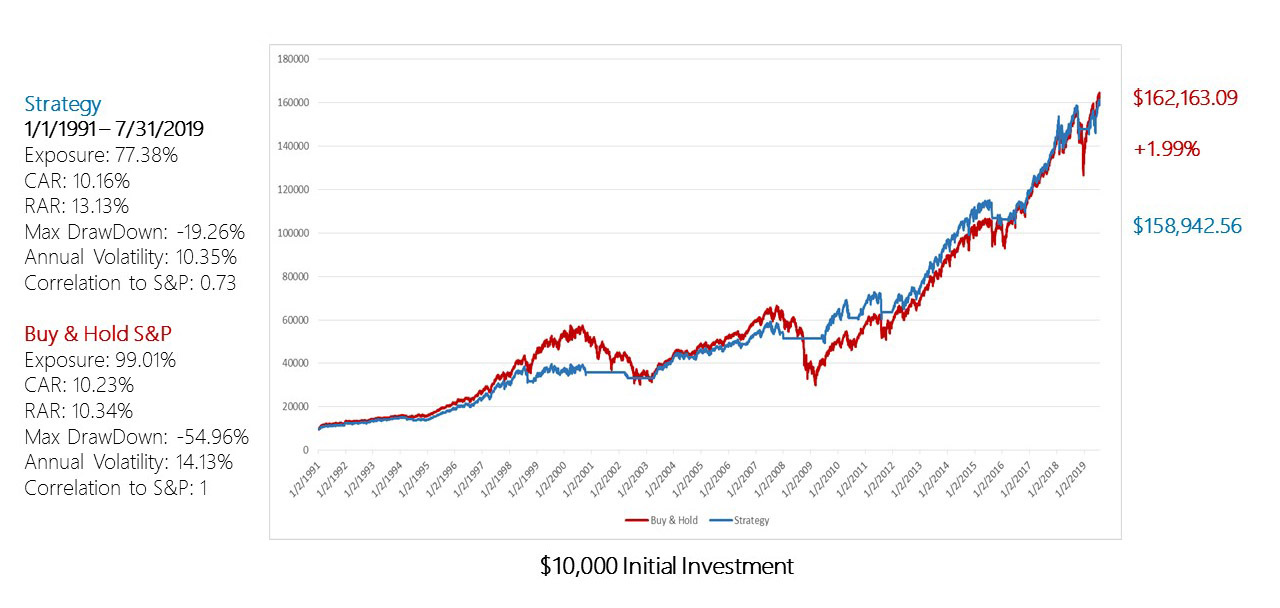

1/1/1991 – 7/31/2019

If we shorten the period to January 1, 1991 through July 31, 2019, the strategy comfortably outperforms the Buy&Hold strategy by 3 points.

Our proprietary strategy’s RAR=13.13%, while the S&P500’s RAR=10.34% and the Buy&Hold has a substantially higher standard deviation and drawdown.

Past performance is no guarantee of future returns.

Key

CAR: Compounded Annual Return is the rate of return, usually expressed as a percentage, that represents the cumulative effect that a series of gains or losses has on an original amount of capital over a period of time.

RAR: Risk-Adjusted Return defines an investment’s return by measuring how much risk is involved in producing that return.

Max DrawDown: An indicator of downside risk over a specified time period

Annual Volatility: Volatility is a measure of the variance of returns over a period of time. As with returns, volatility can be annualized to help provide this frame of reference and give some perspective. To annualize volatility, it’s necessary to measure volatility over a shorter period of time and extrapolate it over the course of a year.